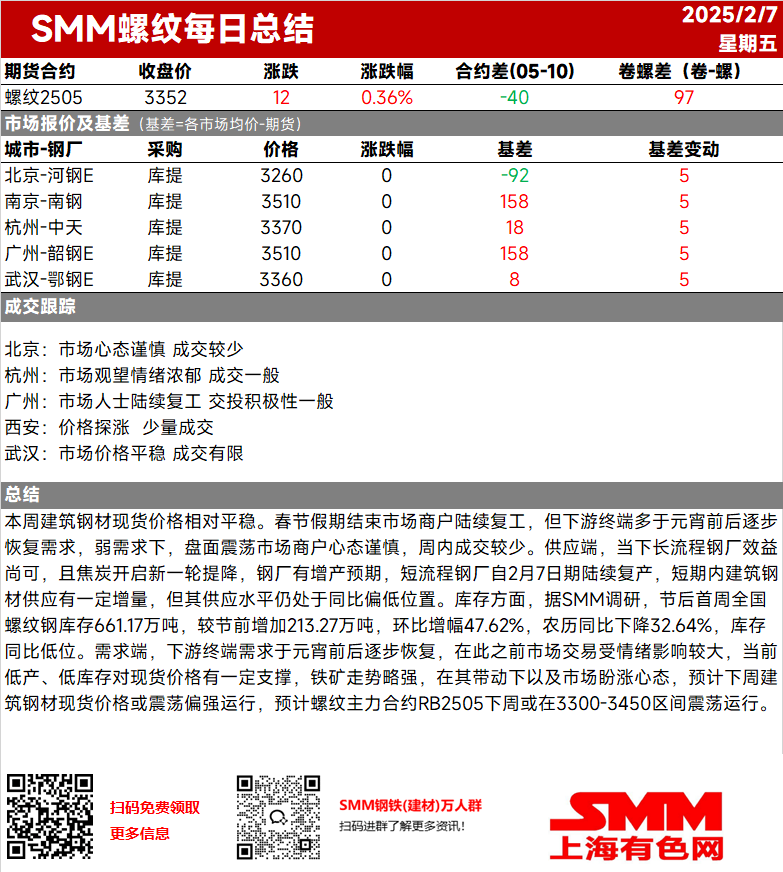

Tuần này, giá thép xây dựng giao ngay duy trì tương đối ổn định. Sau kỳ nghỉ Tết Nguyên đán, các thương nhân thị trường dần dần hoạt động trở lại, nhưng nhu cầu sử dụng cuối từ hạ nguồn dự kiến sẽ phục hồi dần vào khoảng Lễ hội Đèn lồng. Trong bối cảnh nhu cầu yếu, thị trường kỳ hạn biến động, và các thương nhân thị trường vẫn thận trọng, dẫn đến giao dịch hạn chế trong tuần. Về nguồn cung, lợi nhuận hiện tại của các nhà máy thép lò cao ở mức trung bình, và một đợt giảm giá than cốc mới đã bắt đầu, dẫn đến kỳ vọng tăng sản lượng. Các nhà máy thép EAF đã dần dần khôi phục sản xuất từ ngày 7 tháng 2, dẫn đến nguồn cung thép xây dựng tăng nhẹ trong ngắn hạn, mặc dù mức cung vẫn thấp hơn so với cùng kỳ năm trước. Về tồn kho, theo khảo sát của SMM, tồn kho thép cây quốc gia trong tuần đầu tiên sau kỳ nghỉ đạt 6,611,700 tấn, tăng 2,132,700 tấn so với mức trước kỳ nghỉ (tăng 47,62% so với tháng trước) nhưng giảm 32,64% so với cùng kỳ năm trước theo lịch âm, với tồn kho vẫn ở mức thấp so với cùng kỳ năm trước. Về nhu cầu, nhu cầu sử dụng cuối từ hạ nguồn dự kiến sẽ phục hồi dần vào khoảng Lễ hội Đèn lồng. Trước thời điểm đó, giao dịch thị trường bị ảnh hưởng nhiều bởi tâm lý. Hiện tại, sản lượng thấp và tồn kho thấp cung cấp một số hỗ trợ cho giá giao ngay. Giá quặng sắt cho thấy sự tăng nhẹ, và được thúc đẩy bởi điều này cùng với kỳ vọng tăng giá trên thị trường, giá thép xây dựng giao ngay dự kiến sẽ dao động tăng vào tuần tới. Hợp đồng tương lai thép cây RB2505 được giao dịch nhiều nhất dự kiến sẽ dao động trong khoảng 3,300-3,450 vào tuần tới.